.png)

As a startup, a company credit card is a low-lift way to pay your expenses.

But when it comes to finding the right one, keep in mind your startup's unique needs. You don't want a typical SMB's credit card.

You're not a typical SMB. You're cooler than that.

With a typical SMB, spending limits are determined by the business's credit history. But since startups are newly established and have no significant credit history, their spending limits have to be based on something else. The usual card options can't do that.

Brex and Ramp are two options that do things differently: they analyze a startup’s funding, performance, and bank balance to establish credit limits. Brex and Ramp are frequently cited as two of the best cards for startups because of their generous spending limits and lack of a personal guarantee.

Let’s look at how these credit cards compare to other, more traditional options and discuss the features you need to consider before deciding which one to use.

If your startup is venture-backed, you'll want to look for cards designed for companies with capital.

Be aware that spending and credit limits will be linked to a person, not the business.

Here are some other factors to consider:

A small business owner who owns 100% of the company would naturally anticipate receiving benefits for personal travel.

However, venture-backed start-ups should concentrate on selecting a credit card with benefits that assist in lowering burn.

Without much credit history, startups need specialized credit cards for expenses.

But due to a lack of good options, startup businesses often begin by using one of the founders' credit cards.

This might seem reasonable — at first.

Even if it's not reasonable, as a founder, you're used to taking risks and doing what it takes to make it happen.

(I get it. I'm also a founder. Sometimes you have to push.)

A lot of the companies we work with get startup or venture capital funding and then quickly outgrow the credit limit (and other characteristics) of the founder's personal card.

Stop doing that.

Brex and Ramp are good options. Let's talk about why.

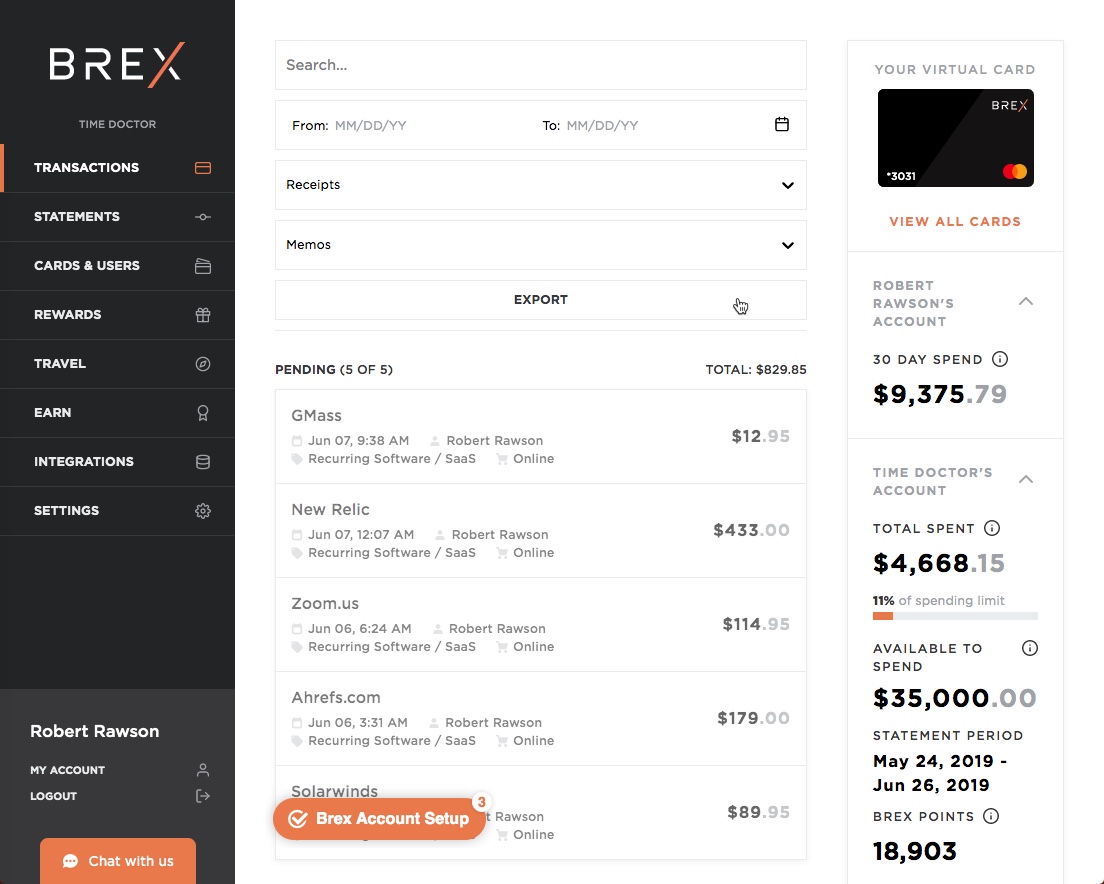

Brazilian businessmen Henrique Dubugras and Pedro Franceschi co-founded Brex in 2017. They understood how challenging it was for startups to get corporate credit cards — due to their limited credit track record.

So Brex provided startup companies with credit cards based on their funding and bank account balances.

Brex could connect to a bank through an API and periodically check a company's account balance in the background. They could then use this info to determine credit card eligibility.

Eric Glyman, Karim Atiyeh, and Gene Lee founded Ramp in 2019. They looked for opportunities to improve Brex's playbook by focusing on UX and UI.

Ramp concentrates on providing exceptional customer service.

Additionally, Ramp wanted to make advancements in user interface, so they included new functions like vendor management.

Ramp appeals to funded startups that want excellent user experience, cost management capabilities, and significant cash back returns.

It depends.

You raised venture capital money to avoid worrying about losing your assets if the startup fails. Don't take on personal liability for your company's debt.

Avoid personal liability by using Brex or Ramp

Brex and Ramp were primarily created to offer credit card options for backed startups. They both:

You want credit cards that can link with QuickBooks for easy bookkeeping. Both Brex and Ramp integrate easily with Netsuite and Quickbooks.

You also want a card that can grow with your financial operations. It should include features like departments or be able to link purchases from specific cards to specific accounts.

A funded startup will likely hire employees much more quickly than a typical small business.

But if everyone on your team uses their own credit cards and submits separate expense reports, your finances can get complicated. It might be difficult to control spending once your team starts expanding.

Expansion still requires advertising, new machinery, and office supplies.

What should you do?

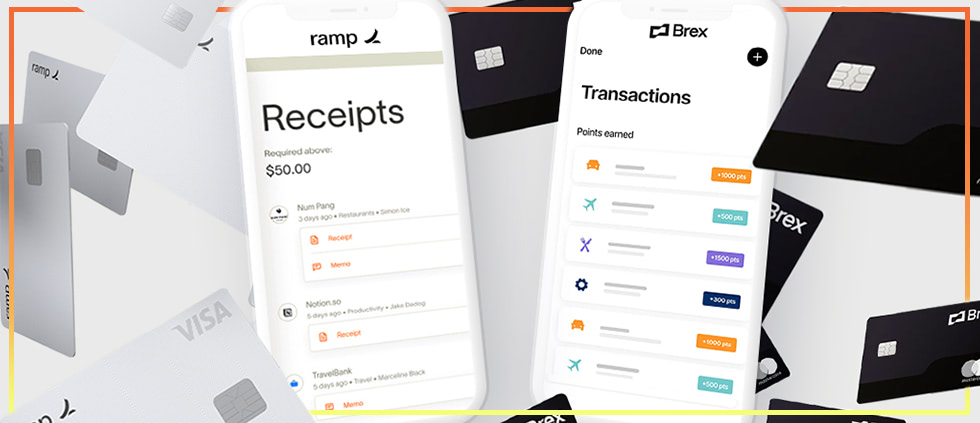

Brex and Ramp provide both physical and virtual credit cards. This lets you easily make purchases both in person and online.

In addition, Ramp and Brex don't allow businesses to have any outstanding balances on their accounts. Since your startup's spending limit is based on its bank account balance, a large balance will negatively impact your ability to qualify for more credit.

So what is the best credit card — Brex or Ramp?

It depends.

In terms of general spending cards for startups, these two stand out as market leaders.

But between the two, the best one still depends on your needs.

Ramp is known for UX and UI. Ramp credit cards are also good at handling international travel due to their higher spending limits.

But Brex has been around a little longer, has a more developed system, and unifies everything into a single screen. Brex can also function as a bank account, making it a complete solution for many commercial banking needs.

What I'm trying to say is... you really can't go wrong with either option.

Once you choose a credit card, you may decide you need some help getting started. You can use Fondo's all-in-one accounting platform to manage your corporate taxes, tax credits, and bookkeeping.

Get your financial reports, taxes filed, and cash credits with Fondo. Sign up today!

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat. Aenean faucibus nibh et justo cursus id rutrum lorem imperdiet. Nunc ut sem vitae risus tristique posuere.

Built for Delaware C-Corps. Trusted by 2,000+ startups.

Copyright © Fondo (BloomJoy, Inc.)

%2520(1).png)